Ep. #7 - Books Every Real Estate Investor Should Read

Show Episode Transcript

Do you read books? If so, are they Fiction books; or do you read Business, Finance and Mindset books? You see I went for a very long time without reading any books. I was a Web Programmer, so I would often read books on Programming PHP, Perl, ColdFusion, JavaScript and other scripting languages. But once I had found what I needed to know to solve whatever coding challenge I was facing at the moment – I put the book down and did not touch it again until some other challenge arouse. I used them more as reference manuals than anything else.

So one year I was away at a business conference, sharing a room with a colleague and he was listening to a Mindset book, which I referred to as a “Self-Help” book – as I asked him “why are you listening to that!?” – Somehow I had developed a negative outlook on such books. I pretty much considered it beneath me to read or listen to such non-sense. I’ve since apologized to him for my comments, as now I try to read a different book on Mindset, Business or Finance – at least monthly. I absolutely LOVE these books, and they’ve helped me greatly to excel in Business but also to improve as a Person in general.

I had learned, as the quote says…

“Reading is essential for those who seek to rise above the ordinary.” – Jim Rohn

Or how about this…

“The more that you read, the more things you’ll know. The more that you learn, the more places you’ll go.” – Dr. Seuss

Welcome to Episode #7 – Books Every Real Estate Investor Should Read.

I absolutely love quotes, so here’s another for you… “If we encounter a man of rare intellect, we should ask him what books he reads.” – Ralph Waldo Emerson

Now not to suggest that I’m a man of rare intellect, but hey – If I don’t think highly of myself – who the hell will? So I remain my biggest fan!

In this episode, I’ll relate some of the books that I’ve read and feel worth you reading as well – as they benefited me greatly, so maybe the same will be true for you also.

To this end, a new page is now live on the [… and Landlord] Podcast Website at: andLandlord.com/books -and here I’ll post details about each book that I mention on the Podcast, along with a link to where you can order the book or get it on Audible.

So in Episode #2 – I mentioned the book Rich Dad Poor Dad by Robert Kiyosaki. This book is cited possible more than any other by Real Estate Investors as the book that got them interest in and into the business of Real Estate Investing. Not that its the best book ever written on the subject of Real Estate Investing… I wouldn’t even say that it is a book about Real Estate Investing necessarily. However, it sets your mind on a different track when it comes to Money, Business and Investing – and it uses Real Estate as an example of the type of thing one SHOULD invest their money in… Because its an asset that produces an income (rent from tenants), tends to appreciate in value and is highly tax favored by the government – among many other reasons.

And then in both Episodes #4 & #5 – I mentioned the second book by Robert Kiyosaki – The Cashflow Quadrant. This is my personal favorite in the Rich Dad series; however, I believe there are a few (including his latest) that I’ve yet to read. I like this book because it talks about the different ways we all get our money, divided into 4 “Cashflow Quadrants”. I’ll not go into that again here in this Episode, but listen to Episode #5 especially, for full details. But in short, this book helped to open my eyes as to the differences in being an employee, small business owner or self-employed (on the left side of the Cashflow Quadrant); versus getting income from a business and investments (on the right side). Its a great read to get you thinking along the lines of diversifying your income and creating a situation where money and systems are working for you, instead of you working for money.

The [… and Landlord] Podcast Books page at: andLandlord.com/books – will grow over time to contain many book recommendations. However, today I’d like to speak about two in particular, that you can find now on this page along with Rich Dad Poor Dad and The Cashflow Quadrant both by Robert Kiyosaki. They are “The 4-Hour Workweek” by Tim Ferriss; and “The Richest Man in Babylon” by George S. Clason.

The 4-Hour Workweek is a book about getting out of the 9 to 5 job trap… How to get out of the cubical and stop working for money to create a situation where you’re leveraging businesses, people and money – to work for YOU. It is exactly the sort of book you should read after Rich Dad Poor Dad and The Cashflow Quadrant, as these two put you in the mindset of making major changes in your financial life – but they are short on actionable advise. What to do… How to do it? Whereas The 4-Hour Workweek is packed with actionable advise that can allow you to create a plan of action, and to start making actual changes in your financial life – by changing the way you make your money.

Go to andLandlord.com/books and click through to the page on The 4-Hour Workweek. There you’ll find my comments on what this book did for me. Unfortunately, I found it a bit late along my path, but it still had a major impact on my course of actions as I worked to remove myself from being involved in almost everything that happened in my businesses. After-all, you can’t create a 4-Hour Workweek for yourself when everything depends on you.

And then The Richest Man In Babylon is a book that is nearly 100 years old; and even more so, it features stories (or parables) set in ancient Babylon, over 8,000 years ago! Why should you bother to read such an old book containing apparently even older stories? Because the stories teach a financial lesson that is just as valid today as they were 100 years ago or even 8,000 years ago for that matter.

Among other lessons, The Richest Man in Babylon teaches “The Seven Cures for a Lean Purse” and “The Five Laws of Gold”. Now you’ll have to get beyond references to things like “purse” and “gold” and just hear and think “wealth” and “money”. You’ll also have to get past all the thee’s and thou’s and other aspects of Biblical speak – but it only helps to take you back in time so the stories really take hold.

These stories will stick with you – for the good. I still think about the “4th Cure for an Empty Purse”, “Guard thy treasures from loss” – whenever I’m about to make a new investment property purchase, go into another area of business or start a new business partnership. I don’t want to be one of those people who amasses millions of dollars only to lose it all in a bad investment or two. This book will not only help to protect you from that sort of outcome, but it will help to build your wealth to begin with.

So remember to checkout the Website at: andLandlord.com/books – which now has these 4 books listed, and we’ll be adding more as they are mentioned on each future episode of the Podcast. And while this episode was all about books, in future episodes we’ll just mention related books and post them to this page or we might do short book segment within the Podcast.

And I don’t want to leave you in complete suspense as to what the full list of books is going to be, so I’ll just mention a few more of them now. In no particular order, some of the additional books will be…

Secrets of the Millionaire Mind

The E-Myth Real Estate Investor

The E-Myth Revisited

Think and Grow Rich

Rich Dad’s Who Took My Money?

The ONE Thing

The Book on Investing In Real Estate with No (and Low) Money Down

The Book on Managing Rental Properties

The Millionaire Real Estate Investor

Extreme Ownership

Never Split the Difference

Pitch Anything

Pre-Suasion

Psyched Up

Influence

And the classic…

How to Win Friends & Influence People

Now as I go through additional Podcast episodes, each of these books will be mentioned as it relates to the topic at hand, or some experience I had. Or something that I think would be beneficial to you in your journey to becoming a Landlord, or to becoming the best Landlord you can be. Real Estate Investing and being a Landlord entails many different aspects of Mindset, Business and Finance. So all of these books play a role.

You’d be surprised how a book on time management, or efficiency, can make your landlord business so much more streamlined and efficient, helping you to put in policies, procedures and systems that take burden off of you, placing it elsewhere, and freeing your time, while still doing an excellent job for your customers, which are the tenants, so that you can grow your portfolio without creating stress, bringing more people onto your team, working with more vendors, more contractors. And as you bring these people in, and your company grows, and you have more employees, it’s only going to make everything run just that much more smoothly if you’ve read a book like How to Win Friends & Influence People or Extreme Ownership. And you know that if your company isn’t working like you want it to, it’s not your employee’s fault. It’s your fault, because either you haven’t communicated to them properly, or you haven’t trained them properly, or you hired the wrong person. A book like Extreme Ownership will help you internalize those things, so that you can get the best out of yourself, so that you can, in turn, get the best out of everyone around you.

These books have an enormous impact on all aspects of your business, of your life, of your finances. As i read them myself, I’ll make them available to you, letting you know what I got from them, what it did for me. And so, I created this page at https://www.andLandlord.com/books, to be that destination where you can go to see what I’m reading, and what you might want to read and why. Now, in full disclosure, if you order a book from that page, I do get a small affiliate commission from Amazon. It’s nothing much, but every little bit helps lessen the expense of producing this podcast.

So, if you listen to the podcast, and you’re going to get the books anyway, I would certainly appreciate it if you get them from https://www.andLandlord.com/books.

So let’s end this episode on Books Every Real Estate Investor Should Read with some final quotes…

“If you are going to get anywhere in life you have to read a lot of books.” – Roald Dahl

And…

“Once you have read a book you care about, some part of it is always with you.” – Louis L’Amour

In the latest Episode (#7), I announce the new [... and Landlord] Podcast Book Recommendations page at: andLandlord.com/books. The various books mentioned mainly concern Property Investment, and should be read by all looking to successfully enter into the Rental Real Estate Investing market.

Books have played a critical roll in my Real Estate success since starting in 2015. I previously had a negative outlook towards so-called "Self-Help" books, or those on Mindset, Business or Money & Finance. But once I actually allowed myself to read the first, I was hooked.

As I've expressed before, that book was Rich Dad Poor Dad, and it changed the way I looked at both money and myself. Some time later I read Rich Dad's Cashflow Quadrant, and it changed the way I looked at my business and how my wife and I made our money as an employee and self-employed small business owner.

I don't remember exactly, but I'm pretty certain my finally reading Rich Dad Poor Dad was a result of listening to the BiggerPockets Podcast, where at the end of each show they ask the guest for book recommendations - and almost every person mentioned this book... So I had to read it! And thus naturally, I started reading the other recommended books also.

Now I'd like to return that favor by not only recommending books that I found valuable, but also providing details into WHY. On the [... and Landlord] Podcast Website at: https://www.andlandlord.com/books - you can get a listing of my favorite books that I feel every Real Estate Investor should read. But also I'll give some details of where I was along my journey when I encountered each book, what I took from it, and what it did for me - so that maybe you may benefit as well.

In this episode of the [... and Landlord] Podcast, I focus on two... The 4-Hour Work Week & The Richest Man in Babylon. Going forward I will speak briefly on others. And I welcome your comments on my recommended books, and your own book recommendations as well.

Now in full disclosure, each of these book recommendations link back to my Amazon Affiliate account - so I do make some coin when you order a book by following a link from this site. But that just helps to offset the cost of the Podcast, and therefore it is greatly appreciated.

Ep. #6 - Evaluate, Market, Negotiate & Fund - What It Takes To Succeed As A Real Estate Investor In 2019

Show Episode Transcript

In 2019, maybe more than ever before - you need to be able to evaluate properties, market for deals, negotiate with sellers, and have reliable funding in place to close. As I've mentioned before, I started my Real Estate Investing career in 2015, which admittedly was a better time to have started than 2019. In fact, I'd say I was about 5 years late. Had I started in 2010, its possible I'd have 10 times the number of properties as I do now. But like the Chinese Proverb says...

"The best time to plant a tree was 20 years ago. The second best time is now."

Welcome to Episode #6 - Evaluate, Market, Negotiate & Fund - What It Takes To Succeed As A Real Estate Investor In 2019...

Having started my Real Estate Investing career in 2015 instead of 2010, I'll try not to lament only catching the tale end of what may prove to be the greatest opportunity to acquire deeply discounted properties in mass that may occur within my lifetime. Likewise, YOU should not use the current market condition as an excuse NOT to get started or to grow in YOUR Real Estate Investing business in 2019.

Sure, 10 or 20 years ago would have been a better time to start, but would you say that someone just turning 18 now (so they were only 8 years old 10 years ago) has missed the Real Estate train due to their "bad timing of birth?" - and so they should not even bother with Real Estate Investing now? Of course not!

Regardless of the decade or year; irregardless of the current market condition - (and what is the difference between "regardless" and "irregardless" anyway? Nevermind...) - THERE ARE ALWAYS OPPORTUNITIES in Real Estate! You just need to know how to recognize them, how to take them down, and how to perform to profit.

This requires certain skills - but the good news is that it can all be learned... So how do you go about finding and acquiring rental property deals in a market like what we have today - where everything appears to be overpriced (at least from a positive cash-flow prospective)? At the start I said... In 2019, maybe more than ever - you need to be able to evaluate properties, market for deals, negotiate with sellers, and have funding in place to close.

So let's start with evaluating properties... Among other things, I've spent the last 4 years learning how to evaluate properties. Remember that one of the key indicators of a potentially good rental property deal is where the likely monthly rent is > 1% of the purchase price + any rehab needed and other expenses. So if you are buying it for $80,000 and it needs $15,000 of rehab to be rental ready, with maybe another $5,000 for closing, holding and other costs, totaling $100,000 all-in; then you'd want to be able to rent that property for $1,000 or more per month. That's called the 1% Rule and it's a strong indicator of a likely great deal - or at least certainly worth your further consideration.

Now from 2010 to 2015 and a few years thereafter, you could almost throw a rock and hit a 1% deal in most markets - they were all over the MLS. It was not even uncommon to find 2% deals, and I've heard of some people bragging of 3% deals or better that were just been sitting on the MLS for months. My personal best is just a little over 1.5%, but my properties also tend to appraise (post-rehab) far above what I had in them, thus allowing me to pull out most (if not all) of my cash upon refi; and in many cases also pull out a nice profit for myself; having equity remaining in the property; and also still maintaining positive monthly cash-flow.

What this means for you is that while the 1% Rule is a great rule-of-thumb consideration, it does not represent the sole-method of profiting from rental property. There are certainly times when it makes perfect sense to buy a property that is < 1% on the rent to cost consideration. The lowest I've gone is just above 0.6% - but I also have no cash remaining in that property (thus an infinite return); pulled out additional cash as profit at refi (free money, tax free); have a ton of equity remaining in the property (I refinanced at 65% LTV); got great tax benefits (due to the expensive rehab finishing the attic into a second 2BR unit); and it sits in an ideal location with progress all around (so massive appreciation potential). I also got the vacant lot next door where we start construction next month on a home with $300,000 comps all around. With all those benefits, do I really care that it failed to meet the 1% Rule? So don't treat the 1% rule as if it were written on stone tablets coming down from a mountaintop held by an old man with a white beard.

If you want to find good deals in 2019 you'll need more than a strict adherence to the 1% Rule. And in that regard, if you're new to Real Estate Investing, you may even be at an advantage over those who started earlier like myself, as my business partner has to remind me all the time (when we're evaluating deals) that it's not 2015 anymore. For example, its hard for me to even think about paying over $100,000 for a 2BR Townhouse, when from 2015 to 2017, I was buying them for $60,000 - and now they're going for twice that and even more. I have to be reminded to take off my 2015 glasses and see things for how they are TODAY. I've missed out on a lot of properties for this reason, as others are able or just willing to pay more than I am.

You see, everyone has different circumstances... I've recently lost deals to persons who paid what I consider to be ridiculous prices for properties that cannot possibly yield positive cash-flow at what they paid. However, maybe they're in a 1031 Exchange, and the alternative to paying too much for the property is getting hit with a massive tax bill. Better to over-pay for a property than to give the same money away to the government and have NOTHING to show for it. Or maybe they are paying all cash; whereas I must account for the cost of financing. Or maybe they are going to live in the property for a year or more, so they are getting much better financing and low to no down-payment; whereas I must put down 20% and my interest rate may be a point or two higher. Maybe they are going to do most of the work themselves and thereby building sweat equity in the property. Or maybe they are just going to knock the current building down (I'm seeing a lot of that in Durham) and build something new that changes the value proposition entirely. So what one person can pay for a property and have it still be a good investment may be entirely different (more or less) than what you or I can pay for the same property due to differences in our circumstances.

So you'll need to understand all the various means by which you can profit from a given rental property to know if you should buy it despite not having the best rent to cost consideration. Can you add square footage (up or out) to increase the value at refi and resulting cash out? Can you steal space from elsewhere in the house to create an additional bedroom of reasonable size to boost the value and rental rate? Is the property at a location that is almost certain to appreciate - highly distressed but ideally located, maybe in an improving downtown area? Can it be torn down for the land to then build something more valuable for the location? Now some of this gets into more speculation than I'm willing to indulge for myself (I'm an investor, not a speculator), but you may be more risk tolerant than me.

These are all different considerations when evaluating what a property may be worth paying for, as you have to be able to justify paying the prices that properties are going for in 2019... How are you going to make any money!? And will you regret what you paid or even be upside down come the next downturn in the economy? Or will it even matter at all if you still have positive cash-flow?

Now this all assumes that if you are going to be rehabbing the existing property into a rental, that you know reasonably well what the approximate cost of that rehab will be; what the finished property will appraise for at refi; what it will rent for on a monthly basis; and what other expenses will average, such as: Taxes (which may go up based upon what you paid at the next assessment); Insurance; HOA (if any); Vacancy; Repairs & Maintenance; Capital Expenditures; Property Management; Interest Rates; Points; Fees; Closing Costs; etc... You'll need to have all of this down cold when running your numbers. I'll go more into detail on these in another episode when I dive into how I evaluate properties for the BRRRR method that I use - which stands for: Buy, Rehab, Rent, Refinance, Repeat - which I believe was coined by Brandon Turner of Bigger Pockets. And I think they have a book coming out soon specific to the BRRRR method of Real Estate Investing.

Now let's talk about marketing... Once you know how to evaluate a property for all that its worth (or could be) - you have to learn how to find them... And in full disclosure, I'm still working on that myself. Hey, we'll improve on this together. There are countless ways to market for deals. I've never been one for bandit signs, but you see them blighting just about every street corner anywhere you go... I BUY HOUSES! Well hell, so do I, but I HATE those signs. However, they must work to some extent or people would stop spending money on them. Just say no... I've spent too much money building my "Blue Chariot" brand, to advertise it (directly or indirectly) with cheap signs illegally placed at street corners. I looked into billboards a couple years back, but it was much more than I could justify at that time. I've also looked into advertising on radio and TV, but the timing just wasn't right.

I do direct mail and door hangers, which have gotten me a few properties. And I can't NOT do the online methods of SEO / SEM and PPC, when I own a Website business, so I'm into that with varying levels of success. I really should put more effort into that, as I should logically have top ranking for "Durham I/We Buy Houses" (and related keywords)... I'll have to get to work on that.

I like calling landlords, for rent signs and CraigsList rental listings to see if they'd like to sell, but that's time consuming so I'll need to setup a VA to handle this on my behalf. Lists for divorce, probate, pre-foreclosure, tax liens, evictions, code violations, etc... They all work to an extent. Really, almost everything works if executed properly and consistently. But some of it (like direct mail) takes more money than others. You can easily spend hundreds, even thousands per month on direct mail. I'll do an episode specific to marketing for deals; however, I'd like to invite a successful wholesaler on as guest to speak to their methods.

Speaking of which... How do you think wholesalers are getting deals? If you are in contact with wholesalers and they are sending you properties for consideration, you should consider each one a personal defeat, that you let someone in your market who is not even going to buy the house themselves get it under contract! Then they are going to sell that contract to you, when if you were on your game, you would have found and worked with that seller directly and likely gotten a much better deal for yourself in the process - or at least that is how I feel whenever I get a property lead from a wholesaler. But there's certainly a logic to letting others do what they do best and paying them well for a valuable service of bringing you consistent deal flow. Hey, as long as they are bringing value, go with what works. That may prevent you from needing to become an expert marketer yourself and may even remove some of the need to be a great negotiator.

So let's talk about negotiating with sellers... As I said before, I've spent the last 4 years evaluating deals (buying a good number of them), but the books I'm reading now are often on the topic of negotiation, as it does me little good to be able to evaluate a deal if the ones from the MLS all suck. Having gotten most of my deals from the MLS in prior years, I now realize that to continue my business growth in the current market, I must now go out and make my own deals - BEFORE they hit the MLS or come to me from a wholesaler. But even in that statement, I still feel everything works with the right strategy and proper consistent execution, including the MLS and working with wholesalers - negotiation comes into play in all cases.

Amazing things will happen for your Real Estate business when you can convenience sellers to give you financing or to sell to you on terms like a lease-option, and do so in a manner that does no harm to (and actually benefits) the seller. To date I've done 3 lease-option deals where everyone benefited greatly, and those sellers now offer testimonials and references as to my ethics in business and personal character - which will just make the next such deal even easier, when I can put that person on the phone with 3 others who've done similar deals with me in the past.

I'll speak more on these and other books and my work to become a better negotiator. One such book is Psyched Up (How the Science of Mental Preparation Can Help You Succeed) by Daniel McGinn, which relates especially well to me, as I've always had a fear of public speaking and presentations. When I went into the house to speak with the first sellers who did a lease-option deal with me, I had to devote a considerable portion of my thoughts and efforts to just not shaking as I explained how it all worked - as I was just that nervous. But by the third lease-option deal I was fine, which built confidence for my first presentation to a Private Lender.

So now let's talk about the money... Most people think you're not going to buy anything if you don't have any money - and so they rule-out Real Estate Investing as something they can pursue, as they think instinctively that to buy a $100,000 house, naturally you need to have $100,000. But this same person would not think twice about going to a car lot and buying a $10,000 or $20,000 car with no money down... Something about that extra zero creates a disconnect for most people that they cannot easily breach. And even when the extra zero isn't there, such as for a $60,000 house, in 2019 they are harder to find and/or just may not be in an ideal location; or needs so much rehab work that you're right back in that 6 figure zone with the extra zero coming into play again.

So let me start by saying that if you can barely pay your existing bills; do not own your own home; have no money in the bank, no savings (no retirement, no insurance); and your combined score from a few frames of bowling is higher than your credit score - you may not be ready for Real Estate Investing (just yet). In that case I suggest you start listening to Dave Ramsey or Susie Orman and get your financial life in order. They provide great advice for that. Because while you may not need a lot of money to be a Real Estate Investor, it helps to have some - and it is even more important to be able to show at least some recent history of managing well what money you do have.

Unless you have some special circumstance, you're likely to need about $5,000 to maybe $30,000 of available funds for down-payment, fees, closing costs and reserves. This can be cash in the bank (ideal), or a Home Equity Line of Credit (HELOC), a loan from a retirement account (IRA / 401K), etc... And your credit score will likely need to be somewhere in the 700 range for the best rates, but some lenders will go lower. You'll also likely need to be some distance in time away from your last late payment, judgement, lien or bankruptcy. But this all relates to your first purchase or maybe your first few using conventional funding, such as from a bank.

You can lessen or eliminate most (if not all) of these requirements, by using 100% OPM - Other People's Money. In the beginning, OPM will likely come only from family and friends - as their love for you may overcome the reluctance to fund what is your first time Real Estate endeavor. But you may also find a seller willing to offer some period of 100% seller financing or a lease-option - it happens, and you won't know if you don't search (market for deals) and ask (negotiate).

But the real fun is once you've established yourself as a knowledgeable and trustworthy Real Estate Investor - because then OPM will come from those who were strangers just days, weeks or months before. It is also when sellers are most likely to be willing to sell to you on terms, which might include 100% seller financing. Further, it is when Hard Money Lenders (aka Professional Private Lenders) will bend over backwards to give you the best terms on money for your deals.

Once you have a few Private Lenders and a Hard Money Lender or two on your team, along with a few conventional lenders, each day that you wake in this business feels different, as your biggest problem is no longer finding money for deals - it is finding the deals in the first place. And then the dilemma shifts from concern about finding money to buy properties to finding enough properties that meet your criteria to keep your Private Lender's funds in-use.

You don't want to have funds committed to you by a lender and not be able to find suitable properties to leverage those funds continually. You'll also have Hard Money Lenders calling and emailing you each week to ask if you've found another property yet. So this becomes the primary reason for needing a highly effective marketing machine and then being able to negotiate win/win deals with those potential sellers. I'll have a future episode about finding and working with Private and Hard Money Lenders - and there's a great book on the topic called "Raising Private Capital (Building Your Real Estate Empire Using Other People's Money)" by Matt Faircoth of Bigger Pockets.

So how do you become and grow as a Real Estate Investor in 2019? YES, its much harder than it was from 2010 to 2018... You'll need to be able to evaluate deals properly, quickly and from a number of perspectives. You'll need to be a proficient marketer to find properties (off market deals) to evaluate and buy. And once your marketing efforts are bringing you a steady stream of deals to evaluate, you'll need to be able to negotiate effectively with those sellers to take the deals down at a price that creates a win/win for YOU and the seller. And regardless (or maybe is it "irregardless") of all that, you won't be able to buy anything if you do not have your finances and business in order such that banks and individuals are willing to lend to you at rates and terms that make the numbers work.

Your lenders are a part of your team, and on many deals it may seem as if the lender is benefiting more than you are - which is why I seek to become a lender myself. But without the lender there is no deal to be had, as even the richest person does not have enough money to buy every property that comes their way. EVERY REAL ESTATE INVESTOR USES OPM... But outside of family and friends (and often times even then) it requires you to position yourself as a Real Estate Investor who is knowledgeable and trustworthy - as no one has any money they will be OK with losing. People work hard for their money, so it is an immense responsibility when using OPM to fund your deals.

Well, that's it for now... I'll talk more about all these things, but let's bring this episode to a close, as it is already the longest so far. Get into the Real Estate Investing business and if you are already, then grow your business in 2019. And if you have no desire to learn how to evaluate properties, and market for deals, and negotiate with sellers - then maybe you should be the bank for others if you are in a position to do so. Being a Private Lender can be very rewarding. I'll talk more about accredited versus non-accredited investors and ways of adding Private Lenders to your team in a future episodes, but reach out to us at BlueChariot.com/invest - if you'd liked to learn more about being a Private Lender on a coming project by Blue Chariot Properties.

In this Episode (#6) of the [... and Landlord] Podcast titled "Evaluate, Market, Negotiate & Fund - What It Takes To Succeed As A Real Estate Investor In 2019." - I speak briefly on each of these four skills that are especially critical in today's "Hot" market. 2019 has been a difficult year for "deals" on Rental Properties for people like myself who are looking to buy cash-flow positive properties, but it seems to be a great year for sellers. From the buyer's prospective, everything appears to be highly overpriced if there is to be any chance of having positive monthly cash-flow. If you're looking to be one of the successful Real Estate Investors, then it's going to take some extra hard-work and manoeuvring on your end to ensure that possibility!

Prior to this year, most (but not all) of my properties came from the good old MLS, and many were short-sales or foreclosures. Having started my Real Estate Investing career in 2015, there were no shortage of these back then, so I could take my pick - and through 2018 I never had a shortage of properties under consideration at prices that easily met the 1% Rule.

In this episode I explain what the 1% Rule is, and how properties meeting this rule are almost certain to yield positive monthly cash-flow. The problem is - they are so much harder to find in 2019 than they were from 2010 to 2018. Occasionally one may hit the MLS, but you'd better act fast, or it will quickly enter a multiple-bid situation where the price gets bid up well beyond anything that will yield 1% in the rent to all-in cost comparison that is the 1% Rule.

Thus, in this episode, I explain how strict adherence to the 1% Rule may not work as well in 2019... Instead, you'll need to be able to [Evaluate Properties] for other possible methods of profit and return; and understand the circumstances that others may be working within that could allow them to justifiably pay what may seem to be ridiculous prices for a so-called "Investment" Property.

In addition to understanding the full profit and return picture and the motivational factors of others willing to pay more, this episode of the [... and Landlord] Podcast goes into aspects of [Marketing for Deals] so that you'll be in a position of working directly with sellers to obtain a potentially better deal than may be possible once a property hits the MLS. And to this end, I explain that you'll need to be skilled at [Negotiating with Sellers] en-route to obtaining your best possible deal, which may even include some aspect of Seller-Financing or a Lease-Option.

And since you'll not be able to close on even the best negotiated deal if your funding is not in place, in this episode I speak on the subject of OPM (Other Peoples Money) for needed [Funds to Close] - which can be from: Conventional Lenders / Banks; Private Lenders; Hard Money Lenders (aka Professional Private Lenders or Rehab Lenders); the seller (in the case of Seller Financing or a Lease-Option); a HELOC; a loan from an IRA/401K; etc... Being a Real Estate Investor certainly takes money, but it does not have to be YOUR money. So here I speak a little on making yourself credit worthy and otherwise appealing to potential lenders and sellers, such that they may be willing to help fund your deals.

Now these skills are always needed and always have been / will be; however, in a seller's market as appears to exist in many locations around the USA in 2019 - you especially need to have the skills to: [Evaluate Properties]; [Marketing for Deals]; [Negotiating with Sellers]; and have ready [Funds to Close]. This 6th episode of the [... and Landlord] Podcast touches upon each of these points in offering my thoughts on "What It Takes To Succeed As A Real Estate Investor In 2019."

Ep. #5 - Expanding On The Cashflow Quadrant - Diversify Your Income For Wealth & Financial Freedom

Show Episode Transcript

Opening / Quote:

As I've progressed to overcome challenges in business, real estate, and even as a husband and a father, I've come across certain quotes that I found in some way inspirational, or that helped to focus my thoughts on an area of my personality and habits where there was just room for improvement. So, I'd like to begin sharing some of these with you. One that I feel relates well to this episode is most often attributed to Gustavus F. Swift, "Don't let the best you have done so far be the standard for the rest of your life."

Intro:

Husband, Father, Entrepreneur, Realtor, a long list of other titles and descriptions... and Landlord. Welcome to the [... and Landlord] Podcast with me, Jonathan Taylor Smith, also known as J.T. - following a roadmap to Financial Freedom through Residential Rental Real Estate. Welcome to the [... and Landlord] Podcast...

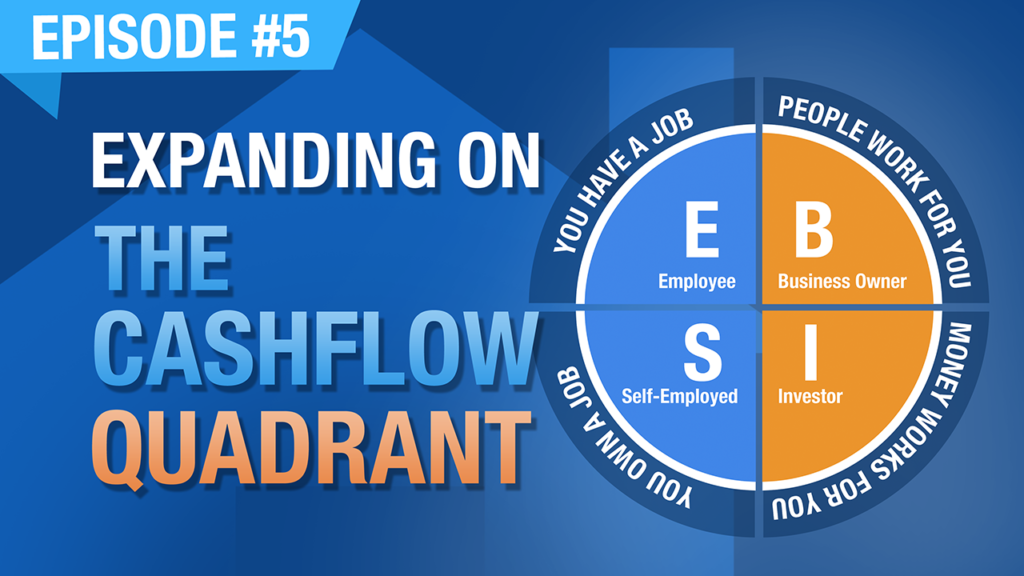

Welcome back, episode number five. So, the previous episode was basically about sacrifice. What are you willing to sacrifice in order to achieve financial freedom? At the start of that episode however I mentioned the second book from Robert Kiyosaki, called the Cashflow Quadrant. My opinion is that it's the best of his books, but you really do need to read the first one, Rich Dad Poor Dad, prior to reading the Cashflow Quadrant. The Cashflow Quadrant is all about how you make your money as it relates to achieving wealth and financial freedom.

And as I mentioned in that episode, it's a circle divided into four regions or quadrants. And the upper left is [E], for Employee, which is where most people get their income. Below that, the lower left is for [S], which is Small Business, or Self-Employed, which is where I get my income. My wife gets her income from the [E] Quadrant, I get most of mine from the [S] Quadrant. Above that, back on the right at the top is [B], for Business. And in his book, he describes it as a business that has more than 500 employees. But as you go further into it, you learn that it really relates to any business that has been systematized such that it runs largely independently of the owner. And I am seriously striving towards that in my businesses. Below that, the lower right corner is [I] for Investor. And that's where we get the other portion of our income, from rental properties and other investments that we have.

For most people, being in the [E] Quadrant, the goal is to spread yourself into those other quadrants until you're entirely out of the [E] Quadrant and you are making all of your money from the [S], [B], and [I] Quadrants. And even better, from the [B] and [I] Quadrants. This relates to the quote that I led with, "Don't let the best you have done so far be the standard for the rest of your life."

If you're currently getting all of your income from the [E] Quadrant, nothing wrong with that. You can get rich in the [E] Quadrant. There are people that have extremely high levels of income from the [E] Quadrant. But it's harder to become wealthy if operating solely in that quadrant. You really need to diversify your income, because when you're in the [E] Quadrant, you're working for someone else. Your destiny is not in your own hands. You need to protect yourself in case the company goes out of business, or they downsize, or you're let go for some reason.

When you're in the [E] Quadrant, you are among the most highly taxed individuals, with the fewest deductions and shelters to protect yourself and limit your tax liability, which is why it is extremely difficult to become wealthy when operating only out of the [E] Quadrant. So, what are you going to do to spread your wings, to move into those other quadrants? Because by doing so, you truly do have the opportunity to change the standard for the rest of your life, to make what you do in the future better than what you've done up to this point.

And that should be taken in no way disparaging as to what you've accomplished up to this point in your life. Remember, I started my first company in 1996. I was self-employed starting from 2002. But I didn't get into real estate until 2015. By anyone's measure, I was successful for that entire period of time. Anyone looking at me would have said, "Hey, he's a successful business man." - I knew that I could achieve more. And so I orchestrated things so that I could move into another area of income, that being investment property, rental properties, and the [I] Quadrant.

And so from that point, with my wife operating in the [E] Quadrant and me being in the [S] Quadrant, we both worked to expand over into the [I] Quadrant with rental property investments and other investments. So, now we're operating in three of the four Cashflow Quadrants. But yet I still know that I have more within me, so I am working to systematize my businesses so that they will truly run without me, putting people in place with the knowledge, skills, and authority to run the businesses on my behalf so that they are viable businesses, not just for a day or a week without me at the helm, but for months, or if necessary, for years. That they will still be viable businesses that operate without me, that bring in cash-flow, that supports my needs financially. That will be financial freedom.

So, my goal is to get entirely into the [B] and [I] Quadrants. For now, I want to operate in all four quadrants. And you know that a table with four legs is far more stable than one with three, or two, or one. If you're only operating in the [E] Quadrant, you have a table with one leg. That's not stable. It's an entertaining circus act, but eventually you're going to fall. So, you need to move into those other Cashflow Quadrants. Add more legs to your table to make it more stable. And the easiest way of doing that is to get your finances set so that you can start buying assets, and investing in things that create cash-flow, that have an income component.

There are other investments that you can pursue, paper investments, stocks and bonds, mutual funds, ETF's. Those things have their place, but that's not what my podcast is about. And that's not what my passion is in. I love rental properties, and being a landlord. And even if you don't want to be a landlord, you can outsource that to a property manager. It's all about putting people, policies, procedures, in place that allow you to be able to get the most out of your day without everything being your responsibility, ultimately building your wealth in the process.

Then in addition to moving into the [I] Quadrant with some sort of investment that creates cash-flow, again, rental property is where I'm at, you need to start a business. Some kind of side hustle. There's so many things that you can do to make money online today. And then even still, lots of businesses that you can start that are in the real world, but can be advertised online. There are opportunities all around to move into the [S] Quadrant. And yes, you're not likely to get rich overnight. Your business isn't going to go live on Monday and you're rich by Friday. You're going to have to work at it. Remember, I started my first business in 1996. I didn't become self-employed until 2002.

So, it took me six years to get to the point where my business was making more money than I was on my day job, and I felt confident to be able to quit, which up to that point was the hardest thing that I have ever done, to quit a perfectly good job thinking that my business was going to be able to provide for me and my family from that moment forward. Scary stuff, but I did it.

So, you don't have to think that your business is going to transform your life overnight. It's going to take work. But what you're doing is you're setting that foothold in another Cashflow Quadrant. You're adding another leg to your table, making everything more stable. And eventually if you do get to that point where your business is making more money, and your time would be better spent on that business than working in the day job, then go ahead and quit the day job, because even though you're, again, removing a leg from the table, the [S] Quadrant leg is far more beneficial to you than the [E] Quadrant leg.

First of all, you are now in control of your own destiny. You're self employed, you have a job that you own. It's your job that you created for yourself, and you are in control of your own destiny. More important than that, as a self-employed individual, as a business owner, you have tax benefits, deductions, and shelters against taxes that can start building your wealth, because when you're in the [E] Quadrant, you earn money, you pay taxes on that money, and then you spend what's left over. But when you're in the [S] Quadrant and the [B] Quadrant, you earn money, you spend money, and you pay taxes on what's left over.

Did you catch the difference? In the [E] Quadrant you pay your taxes first, and then you spend what's left over. But in the [S] and the [B] Quadrants you spend the money first, tax free, and then you pay taxes on what's left over. Now, of course there are some limitations to that. You have certain rules and regulations you have to follow. But the general sense of it is that as a business owner you are expected to have certain expenses for your business. You have to keep your personal and your business finances separate, but to the greatest degree possible you put your expenses on your business. You spend the money before you pay tax on it, and then you pay tax on what's left over.

The difference is transformative for the creation of long term legacy wealth, because taxes are your number one expense in life. Nothing will take more of your money than taxes. And it's not just income taxes, but property taxes, sales tax, and all the fees and everything that you pay taxes on. You don't even realize many of the taxes that you pay. You don't realize how much of the price of something you buy, like a gallon of gas, is actually just taxes.

Taxes are your number one expense in life. And so by moving yourself from the [E] Quadrant to the [S], and then later to the [B] Quadrant, you are creating a wealth effect of tax savings. So, you keep your [E] Quadrant job for as long as you have to. But as quickly as possible you need to move into the other quadrants. And the easiest of the other quadrants to move into, from my experience, are the [S] and the [I] Quadrants. It doesn't take a lot of money to start a business on the side. And it takes far less than most people realize to buy investment property assets.

Like I've said before, you can get a bank to give you 80% of the money. My first rental property, it required less than $20,000 out of my pocket. And that may sound like a daunting figure to many, but there are many ways that you may not be thinking of that you can get $20,000 to buy an investment property. And there are techniques that you can use that might require zero out of your pocket. So, start looking for ways to move into the [S] and the [I] Quadrants. And if you have to keep your [E] Quadrant job while you do that, there's nothing wrong with that. As a matter of fact, there are some scenarios, like the case for my wife, where it makes perfect sense for her to stay in her [E] Quadrant job, especially with what we're doing in the other quadrants, because it won't take very long for her to get to a point where she can retire and will have an income from that job for the rest of her life.

So, why would you quit something like that prematurely, even if you have income from other sources? I quit my job because, well one it was excruciating, I was never cut out to be an employee. But I needed to free my time in order to build my business. But even if I had kept that job, it was not one that would have ever led to any retirement benefits, or anything like that. It would have just been a job that eventually the company went out of business shortly after I quit anyway. Not saying that they went out of business because I quit, but as it would happen, the company went out of business anyway. So, even if I had kept the job, I would have eventually become unemployed. So, I did it on my terms and it worked out perfectly.

So, "don't let the best you have done so far be the standard for the rest of your life". Spread your wings into those other quadrants. Buy a rental property, or some other cash-flow generating investment. And start a business. Something on the side, you don't have to quit your day job. And I recommend it be an online business, because that's where my expertise lies.

I've mentioned before that I had an IT business, a Web Hosting business. Well, let me tell you a little bit about that business. The name is ViUX Systems, Inc, that's V (as in Vision), U-I-X (as in X-Ray). And the website is ViUX.com. And it is a Web Hosting business. What it does is, it helps small businesses and individuals get online and have a website and email, and all the related services that you'd need to do business online. If you've ever heard of GoDaddy, you're aware of what my business does. It's all the same stuff. But whereas GoDaddy has millions of customers, ViUX has thousands of customers.

And when you're seeking to start an online business, I recommend that you begin with the domain name. A lot of companies come up with the name of the business, and then they go out to try to find the domain name, and they end up with a domain name that does not match their business name, or has dashes in it, or it's some extension other than dot COM. And that's not to say the extension has to be dot COM, there are some pretty great extensions that came out a few years ago other than dot COM. But dot COM is still the king, it's still the assumed ending of a domain name.

It means you're going to have to work just that much harder if you don't have a dot COM in order to get it publicly known. So, start with an excellent domain name that matches your business name. Name your business after the domain name once you've acquired it, and try to get one that is an exact match of what you want the name to be, and with the preferably dot com extension. But there are others that you can choose from.

So, with me you'll notice this podcast is the [... and Landlord] Podcast. And I have andLandlord.com. The podcast is brought to you by Blue Chariot Media, and I have BlueChariot.com. I also have BlueChariotMedia.com. The hosting company is ViUX, and I have ViUX.com. Do that favor for your business and get a domain name that matches what you want the business name to be. But before any of that, you have to make up your mind to start a business, to move into the [S] Quadrant. And hopefully you start a business that through additional effort and time in business, and putting policies and procedures in place, that you can move it to the [B] Quadrant.

Regardless of whether you're in the [S] or the [B] Quadrant, the excess income from that business, move it into the [I] Quadrant. Use it to buy investment properties. Buy assets that create cash-flow. So, again, operate in as many of the Cashflow Quadrants as you can. My wife gets her income from the [E] Quadrant, but it makes sense for her to remain there because she has a great job, she gets retirement benefits, and not just that, but she gets the healthcare benefits that our family depends on from her job. I get my income from the [S] Quadrant, and I'm working to move that over to the [B] Quadrant. The money that I make from that business, I save it and I invest it in assets that are in the [I] Quadrant.

So, I have a diversified income structure between my wife and myself. We have three, and working on four legs to our Cashflow Quadrant table, because we're operating in three of the four quadrants. Even if we only had two, we would want them to be on the right side, in the [B] and the [I] Quadrants, because those are the quadrants that will allow us to have other people and systems working for us, rental properties and other investments working for us. Our money working for us, so that the excess cash-flow from those businesses in the [B] Quadrant and those investments in the [I] Quadrant are enough to pay all of our expenses for the lifestyle that we want to life, which is what true financial freedom is all about.

That your business and your investments pay for your lifestyle. That's where we're headed. And so I want you to get there as well, and I want you to start thinking about how you can get into those other quadrants, especially if you're only in the [E] Quadrant right now. And remember, my knowledge of and use of the phrase Cashflow Quadrant in the diagram and everything, it didn't come from me, it came from the book Cashflow Quadrant by Robert Kiyosaki.

From my understanding, it came to him from his Rich Dad, which is from the original book in that series, Rich Dad Poor Dad. I would highly, highly recommend that you go read those books. Start with Rich Dad Poor Dad, and then go to the Cashflow Quadrant book. I think the third in the series, if I'm not mistakes, is one about increasing your financial intelligence. I've also read that, and I'll speak a little bit about that. But read those books. And again, they may not be the best written books, but he will tell you himself, he is not a best writing author, he's a best selling author. So, don't criticize the books for how they're written, or whatever. But utilize them for the content that they contain. The lessons are invaluable, and if you've read them before, as I said, read them again. It has to hit you at the right time in your life when you're looking for that thing that these books can be the answer to that thing you're looking for.

By the fact that you're listening to this podcast, I would suspect you're on a journey leading you towards financial freedom. And if you've gotten this far without reading those books, I'm telling you they were transformational in my life. You should read both of them, starting with Rich Dad Poor Dad, and then go into the Cashflow Quadrant. I'll give you some more information about the other book, about financial intelligence. And there are still more books in the series. But those were the ones that were foundational for me.

And then there's still another book, and that one is The Richest Man In Babylon. Now, Robert Kiyosaki didn't write that book, it's a very old book. I'll give you more details about it. But I will be speaking about that book in a coming podcast episode, because it teaches you how to manage money, and how to save money. And even how to get out of the wrong type of debt, so that you can be successful. And I mentioned the wrong type of debt, because I listen to persons like Dave Ramsey who would teach that you shouldn't have any debt. I personally disagree with that. I think that there are certain debts that you want to have, and certain debts that you don't want to have.

Credit card debt, any other debt that doesn't tie itself to an asset that pays you money is a debt that you want to avoid. But debts like rental property, where the income from the property is paying the debt, there's nothing wrong with that. It's the greatest type of debt you can have. Why wouldn't you want to go out and buy $1 million worth of rental property and have $1 million worth of debt that your tenant pays for? That's the greatest thing ever, why would you not want to do that? That's the best type of debt to ever have.

And so I'll talk more about those types of scenarios as well. All of the books that I mention on the podcast will be available on a books page on the website. I'll upload it at andLandlord.com/books. And you'll be able to click through to get any of the books that I'm speaking of. I'll try to not just put up a list of books and say, "Hey, go read these," but let you know what I took from the book, and how it affected me and my journey towards financial freedom. Because that's what this is all about, it's about using real estate and businesses and other means to achieve financial freedom. And also at the same time, how it should affect your family life.

Like I said, I'm a husband and a father. My businesses and my investments relate to how I am at home with my family. So, it's all about living the best life that you can. I personally think real estate investing and being a business owner is an enhancement to my life. And I simply want to share that with others to give you the opportunity to do the same. And maybe by hearing my story, and those of others I will bring on this podcast, it might streamline your process to get to where you want to be in life.

Exit:

Thank you for listening to the [... and Landlord] Podcast, with me, Jonathan Taylor Smith, by Blue Chariot Media. Following a roadmap to financial freedom through residential, rental, real estate. You can find the podcast website and blog at andLandlord.com. The main company site is BlueChariot.com. If you've received any value from this podcast, help me, please, to make it available to others and make sure you don't miss an episode, by subscribing and posting your five star rating. Plus, share it on social media. I welcome your comments on the blog. And if you'd like to share your Landlord Horror Story, or have a comment or a suggestion for the show, call 844-USA-BLUE - and enter extension 263, which spells "AND" on your keypad (as in AND Landlord). And leave a message. It may be used on a coming show.

Thank you. Be all that you are.... and Landlord.

Disclaimer: Nothing on the preceding show should be considered specific, personal, or professional advice. Please consult an appropriate tax, legal, real estate, financial, or business professional for personal advice. The comments and opinions of any guest are their own. Information is not guaranteed. Any investment may have potential for both profit and loss. The host is speaking solely on behalf of Blue Chariot Media LLC.

In this episode (#5) of the [... and Landlord] Podcast, I expand on something that I touched on briefly in the prior episode (#4) related to Rich Dad's Cashflow Quadrant, which is a book by Robert T. Kiyosaki. In this book he explains the Cashflow Quadrant (pictured within the above image); and in this episode of the podcast, I relate my own positioning within the Cashflow Quadrant and what you may wish to make your goals for the same, along with how to diversify your income - and why.

I highly recommend that you read this 2nd book in the Rich Dad series (after reading the 1st, Rich Dad Poor Dad) - as together, they are greatly helpful in setting the ideal mindset and providing a guide for financial success. When I first read these books (I've since listened to each 3 times), they were exactly what I needed. They focused my thoughts and efforts on a path that I was previously stumbling to find.

I knew that what I had been taught about finances and investing was somehow "off", but these books made it clear as to exactly what was wrong and what I needed to change. I cannot stress more strongly how valuable these books were for me; and I've found that most Real Estate Investors mention one or both of these books as foundational to their success.

This 5th episode of the [... and Landlord] Podcast begins with a quote...

“Don’t let the best you have done so far be the standard for the rest of your life.” - Gustavus F. Swift

This quote relates because I've been seeking and working towards something more for my life since I became an adult almost 29 years ago upon graduation from high school. I'd been an employee since my first job of age 15 at McDonald's - and I HATED every minute of it! I had been able to get steadily better jobs in food service, retail, offices, tech, etc... But I was still an employee, so they were only slightly less excruciating as the jobs improved.

At each step of my employment journey, I was seeking to improve upon this standard to move into something better. And even in 1996 when I started my first business, right through 2002 when I finally ceased being someone else's employee (reaching the level of self-employment) - I was still always seeking to raise my standard for what was to come next.

I established another standard for myself in 2015 when I bought my first rental property, but I did not stop at just one... I'm now beyond double digits - and I want more. To make the quote personal, I refuse to "let the best I have done so far be the standard for the rest of my life" - I can do better! I know that I have it within me to achieve even greater levels of success, ultimately resulting in financial freedom for myself and my family.

In the [... and Landlord] Podcast (Episode #4) - I mentioned some of the things that I had to sacrifice to reach this new standard for my life. In this (the 5th episode), I express this quote and how it relates to the Cashflow Quadrant and my ever changing path (along with my wife) to financial freedom through Employment, Business, Real Estate, and other Investments. Having income from multiple Cashflow Quadrants is essential to growing your wealth and achieving financial freedom.

I express how taxes are the #1 expense faced throughout life for most people, and those who get their income only from the [E] Quadrant are among the most highly taxed. Getting income from the [S] and [B] Quadrants not only provides many tax benefits, but also potentially provides additional funds to buy cash-flow positive assets and investments in the [I] Quadrant. Listen to this Podcast and read or listen to the book Rich Dad's Cashflow Quadrant, to start or focus your path to financial freedom by getting diversified income from multiple Cashflow Quadrants.

Ep. #4 - What Are You Willing To Sacrifice To Achieve Financial Freedom?

Show Episode Transcript

What’s going on, everyone? Episode No. 4! I'm getting into this. I'm starting to enjoy it. So, last week, I did a bonus episode. I did two episodes last week. Don’t know if I'll have time to do that this week, but I'm working on several episodes. So, I'm excited about the content that I'll be able to put out in the near future. Today, I thought I would do an episode about sacrifice. What are you willing to sacrifice in order to be financially free? And don’t get me wrong. I ask that question still on my own journey towards financial freedom.

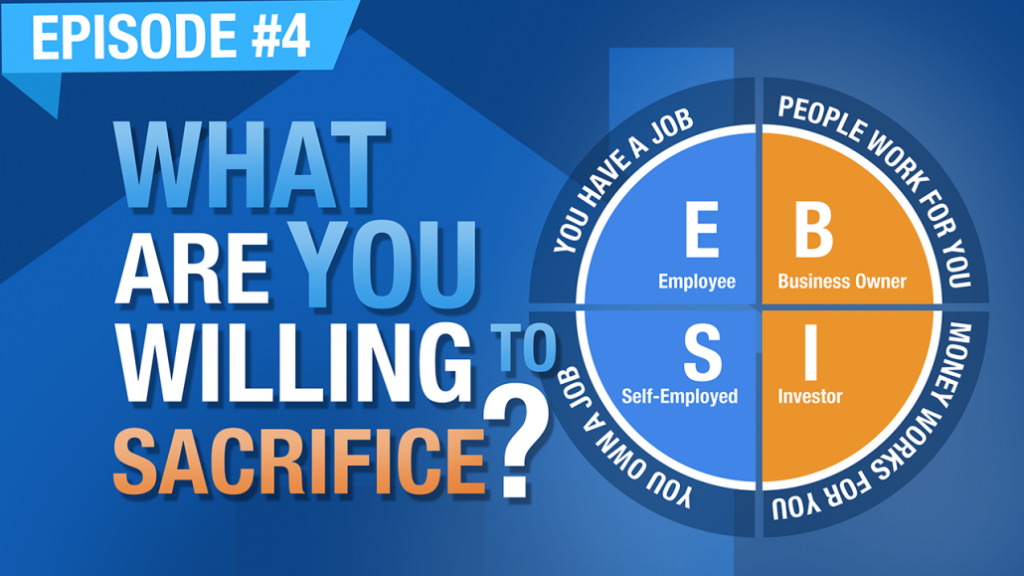

So, I haven’t gotten there yet myself, but it’s in sight. I have a plan that I feel confident will get me there. And the reason I don’t feel I'm there already is because in the reading of what I think is Robert Kiyosaki’s second book, The Cashflow Quadrant, he mentions the four quadrants that a person receives their income from.

And the cashflow quadrant is basically a circle, which is divided into four regions, and the upper left hand corner is [E] for employee, which is where most people get their income from, and that’s the quadrant that my wife’s income is derived from. Then the lower left side of the quadrant, is [S], for self-employed or small business, and that’s where I get my income from. I'm in the [S] quadrant. Back at the top, on the right side, is [B], for business, which Robert Kiyosaki describes that as more than 500 employees, or a business that will continue to run even if you're not there for a prolonged period of time. Below that, the lower right corner, is [I] for investor.

And so, I operate out of three of the four quadrants, with my wife being in the [E], me being in the [S], and she and I together in the [I] through our rental properties and other investments that we have. But we’re not in the [B] quadrant. My businesses, none of them are larger enough. There are no 500 employees in any of my companies. If I weren't there for some period of time, and when I started, especially my IT company, it would not last a day if I wasn't there.

And then as I read books like The 4-Hour Workweek, and Traction, and other books that teach you, basically, how to create a real business that doesn't rely upon you, I was able to put systems and procedures in place that backed off some of that responsibility from my shoulders.

So, now, yes, the business can operate for some period of time without me, but it’s not years. It’s probably not even months. It’s weeks at best. And so, I don’t consider myself to operate in the [B] quadrant, and based on Robert Kiyosaki’s definition, I don’t operate in that quadrant. Even with my investments, they call rental properties ‘passive income’, but they’re only passive to an extent. You do have to do some things to keep the money coming in, and to keep everything from falling apart. And so, they’re not completely passive. And so, until I get to that point where I have enough money coming in from activities that require nothing of me, I don’t consider myself to be financially free. But I do have things in works that will get me there.

So, going back to what I was asking before, what are you willing to sacrifice in order to become financially free? And I ask this because I had to make some sacrifices to get involved in real-estate investing.

Prior to 2015, I was an avid sports fan, and I was a guy who had the NFL Sunday ticket, and I would watch several games on Sunday. I would record several games, and I would be watching those games Monday, Tuesday, Wednesday, and Thursday of that week. This was before there was regular Thursday night football, and I would be watching the Monday night game without trying to find out who won on the games that I recorded. So, I would usually record the Monday night game, and watch it later, and football went throughout my week. Basketball, professional basketball, especially when it got past the all-star break, and when the playoffs come around, I was there every game. College basketball, most games. College football, most games, I pretty much liked every sport with the exception of baseball and hockey. At one point, I was in three different NFL fantasy sports leagues at the same time.

Very confusing to keep up with things, and I watched a lot of television. Sci-fi TV shows and movies, crime dramas, action, a lot of different shows, always watching television. Even when I was working, I would usually have a television on in the background. My excuse was that I am not really paying attention to it. I'm still getting my work done. It’s just something on in the background to keep me entertained. But it took up a lot of time watching television all the time. When I was in my car, I would usually be listening to music, or political talk radio.

When I decided I was going to become serious about real-estate, I cut all of that out of my life, pretty much cold turkey. I quit watching sports entirely. For three years, the only sports I watched were the Super Bowl. The first year, it was just because I was invited to someone’s house to watch it. But other than that, I cut out sports entirely, including all the playoffs. Didn't watch those either. And an amazing thing happened, I kind of lost interest in it. It was like the desire to watch sports just faded away over a short period of time. I became uninterested to the point where when I came across a game, or I would hear somebody saying “hey, such and such game is on”, like Duke and Carolina, or something like that, I was like “huh, well”, I wasn't really all that interested in watching it, which was something that’s unheard off for the former version of myself. I would have planned my entire day, if not a week, around making sure that I was going to be able to watch that game, but I gave that up. Why? It was a sacrifice I was willing to make for real-estate.

Likewise, with regard to television, I watched everything you could think of. We've got like three DVR’s in our household, so there’s plenty of capacity to record all sorts of programs, but I cut it out. The only thing I continued watching were the few programs that my wife and I watched together. So, there’s like that two hour window between 8 and 10 when we’re both in bed, we would watch some program together. I continued to do that because that’s time spent with my wife, laughing or joking about something ridiculous that we’re watching on television.

Other than that, I cut television out of my life, and then music. I stopped listening to music entirely. I completely cut out political talk radio type programs. I realized, ultimately, that it wasn't doing me any good to be up on the latest politics that wasn't pushing my financial freedom goals down the line. So, I killed that as well.

I replaced all of these things that were sucking time out of my day and my week, with reading books on real estate and on business and on mindset, most of all, listening to podcasts. When I'm in my car, that’s what I'm listening to; someone’s podcast. And I hope my podcast can become that for someone else. I would soak up information from podcasts. When I'm at home, I would be listening to books, and again, whenever I say read books, I probably mean listen to. Audible was on all the time in my car, a lot of time at home, when I'm cutting the grass, when I'm working around the house, when I'm cooking dinner, or anything, I'm probably consuming something about business and real estate. Those things that weren't productive to my financial freedom goals, I got rid of them.

So, that’s why I ask; what sacrifices are you willing to make in order to put a plan in a system in place that you can follow that will, ultimately, lead you to financial freedom? Are there things in your life that, while enjoyable, are not really the best productive use of your time? What can you get rid of in your day that doesn't take you away from friends and family, but still allows you to clear time on your schedule for education, for enlightenment, evaluation of what you’re doing now that you can potentially do better in order to become financially free sooner?

For me, it was to get rid of sports, politics, music, and entertainment, right up until the point where it would have also caused me to lose friends and time with family. And that does not mean everyone has a right to be in your life. If there are people, even family and friends, who are detrimental, or even just not supportive of you trying to achieve financial freedom, they don’t need to be in your life.

Limit your exposure to negative influences and move on to better things. I have a very dear friend who lamented the fact that I was no longer able to debate the latest political happenings because I wasn't following it anymore. But I replaced that time with education on real-estate. I wouldn't be able to have this podcast right now if I didn't educate myself over the prior four years on real-estate investing. Everything I'm speaking to you about, and will speak to you about, I learned over that period of time, and I continue to learn now, because of the fact that I replaced non-productive, time-suck pastimes that filled my week with productive time, to educate myself on something that I was passionate about, and that is financial freedom through real-estate investing, specifically rental properties; being a landlord. And that is what brought about the [… and Landlord] podcast. So, what are you willing to sacrifice?

I would submit to you that if you spend any time listening to music, in my opinion, you’re wasting your time. Unless your line of work is somehow in the music business, listening to music isn't doing anything to enlighten you. It’s not doing anything to educate you on finances, or business, or real-estate, or anything.

Watching TV, I would submit to you that Dancing With the Stars is not going to lead you to financial freedom. The Bachelor is not going to make any money for you. Anything with hip-hop, or wives of some profession, or city, in the title, is not going to teach you how to manage finances. Whatever reality show, whatever TV show you spend your time watching, and there are lots of out there that I would really love to watch, they’re not going to make any money for you. I make an exception for a few shows that my wife and I like together because that’s time that we have together to laugh and joke about something. With that exception, and keeping it limited, I don’t watch a whole lot of television. I gave it up, even though there are countless shows on TV that I would love to watch. I think, right now, we’re probably in the golden age of television. There has never been a better time to be entertained on television, or at the movies. But is it going to get you to financial freedom? I would say no.

What are you willing to sacrifice? That is a question that needs to be answered, because it will take sacrifice in order to get to financial freedom. And it’s not just the sacrifice of the things that spend time, it’s also a sacrifice of the things that spend money. Do you spend $6 every morning on a cup of coffee? If you do, I would say you’re wasting money. That could be used to save towards a down-payment on a rental property. There are lots of activities that we undertake every day that we don’t realize how much money they spend.

What I did related to finances, is I bought a program called Quicken, and I started tracking all of my finances in Quicken. It told me, after a very short period of time, what I spent my money on. I could tell you, to the penny, what I spent on for beer, for pizza, and clothing and dry-cleaning. All the different things that I spent my money on, I would enter it into Quicken, and I would categorize it all. Thankfully, because of the fact that I don’t transact in cash very often, it was easy for me to categorize and lay out all of my transactions in Quicken.

And it becomes shocking to see where your money goes, how much I spend at Chick-fil-A, or Bojangles. It was shocking when I looked at it, and realized one year that I spent almost $750 that year at Bojangles, and even more at Chick-fil-A. That’s ridiculous. It was $2000 in fast food I could have put towards a rental property. So, I immediately changed my habits. I sacrificed that apparent desire for fast food, and I stopped going to Bojangles, to the point where I didn't remember the last time I went, because of the fact that I was able to see that it was wasting money going out to eat fast food all the time. And not just there, other places I looked at how much we spent at Olive Garden, and Red Lobster, and Outback. Not just the chain restaurants, but when we would go to places that are better, it was a lot of money being wasted. So, we decided to sacrifice on our eating out budget, and to start cooking more at home. I learned how to cook, because I previously did not, and between my wife and my self, with both of us cooking, it created a lot more leftovers, and it saved a lot of money.

So, look through your schedule. Look through your finances. Put some method in place of tracking your spending. See where you’re wasting not just time, but also money. Re-deploy that time towards educating yourself on business, on real-estate, on finances. Change your spending habits so that you have as much money as possible to invest for your future. Save money so that you can invest that money, so that money then starts working for you. You cannot be financially free only working for money. You have to have money also working for you, and you’re not going to get there if your time is spent on Dancing With the Stars. Don’t let me pick on that. I think I have that in my head because Brandon Turner often uses that as an example on the Biggerpockets Podcast, and I listen to that all the time.

Regardless of what it is that’s consuming your time that’s non-productive, you need to re-evaluate, and re-position, so that you can be financially free. So, ask yourself what are you willing to sacrifice, and then do it, so that you can eventually become financially free.

What Are You Willing To Sacrifice? What are the steps to Financial Freedom?... Yes, it is a buzzword, but it is also a most precious thing to be sought-after with all your effort. And are you really giving it ALL your effort? Are you even giving it SOME effort? Most people think they are, when they really are NOT - or worse, they don't even think about it at all. Which is sad, because you're not likely to stumble into financial freedom. Sure, I buy a lottery ticket here and there, but that's not my plan for financial freedom... That's just me bowing to the 2nd best advertising line in the history of ads... "You Can't Win If You Don't Play". FYI, the best is "What Happens In Vegas Stays In Vegas"; and if you care to know, the worst is "Six Is Greater Than One".

But back to my point... A lottery ticket should not be anywhere in your plan to achieve financial freedom; and if you're going to do so, it will take SACRIFICE. In this episode of the [... and Landlord] Podcast, I relate my personal sacrifices made as part of my plan to achieve financial freedom. My sacrifices included: Entertainment (Sports / TV / Movies); Fast Food & Dining Out - each of these things consumed too much of my time and/or money, so they had to be figuratively crossed-off my daily to-do list, thus largely eliminated from my day-to-day routine. But that was just half of what needed to change. The other side was to replace these time wasters with productivity and learning, plus saving money for investing so that my money could begin working for me.

Instead of watching Football and Basketball, I began listening to Podcasts and reading / listening to books on Business, Real Estate, Mindset, etc...

Ep. #3 - The First 3 Things I Had To Learn How To Do For Purchasing My First Rental Property

Show Episode Transcript

What’s going on, everyone? Episode No.3! Thank you for coming back. This is a bonus episode, the second this week. As I said, occasionally, I would release more than one episode per week. I wanted to elaborate a little bit on the topic from the prior episode which was speaking about my first rental property purchase, a townhouse, that I bought in May, or actually got under contract, in May of 2015, and enclosed on it in July of 2015.

So, I wanted to speak a little bit more about that whole process, some of the underlying things that I had to do in order to get to the point of being able to make that purchase.